Islamic Banking- an Analytical Essay

A.L.M. Abdul Gafoor, Wednesday 8 March 1995

This article is actually Chapter 4 of the book, Interest-free Commercial Banking, by Professor A.L.M. Abdul Gafoor, 1995)

4.0 Introduction

Modern banking system was introduced into the Muslim countries at a time when they were politically and economically at a low ebb, in the late 19th century. The main banks in the home countries of the imperial powers established local branches in the capitals of the subject countries and they catered mainly to the import export requirements of the foreign businesses. The banks were generally confined to the capital cities and the local population remained largely untouched by the banking system. The local trading community avoided the foreign banks both for nationalistic as well as religious reasons. However, as time went on it became difficult to engage in trade and other activities without making use of commercial banks. Even then many confined their involvement to transaction activities such as current accounts and money transfers. Borrowing from the banks and depositing their savings with the bank were strictly avoided in order to keep away from dealing in interest which is prohibited by religion.(1)

With the passage of time, however, and other socio-economic forces demanding more involvement in national economic and financial activities, avoiding the interaction with the banks became impossible. Local banks were established on the same lines as the interest-based foreign banks for want of another system and they began to expand within the country bringing the banking system to more local people. As countries became independent the need to engage in banking activities became unavoidable and urgent. Governments, businesses and individuals began to transact business with the banks, with or without liking it. This state of affairs drew the attention and concern of Muslim intellectuals. The story of interest-free or Islamic banking begins here. In the following paragraphs we will trace this story to date and examine how far and how successfully their concerns have been addressed.

4.1Historical development

It seems that the history of interest-free banking could be divided into two parts. First, when it still remained an idea; second, when it became a reality — by private initiative in some countries and by law in others. We will discuss the two periods separately. The last decade has seen a marked decline in the establishment of new Islamic banks and the established banks seem to have failed to live up to the expectations. The literature of the period begins with evaluations and ends with attempts at finding ways and means of correcting and overcoming the problems encountered by the existing banks.

4.1.1Interest-free banking as an idea

Interest-free banking seems to be of very recent origin. The earliest references to the reorganisation of banking on the basis of profit-sharing rather than interest are found in Anwar Qureshi (1946), Naiem Siddiqi (1948) and Mahmud Ahmad (1952) in the late forties, followed by a more elaborate exposition by Mawdudi in 1950 (1961).(2) Muhammad Hamidullah’s 1944, 1955, 1957 and 1962 writings too should be included in this category. They have all recognised the need for commercial banks and the evil of interest in that enterprise, and have proposed a banking system based on the concept of Mudarabha – profit and loss sharing.

In the next two decades interest-free banking attracted more attention, partly because of the political interest it created in Pakistan and partly because of the emergence of young Muslim economists. Works specifically devoted to this subject began to appear in this period. The first such work is that of Muhammad Uzair (1955). Another set of works emerged in the late sixties and early seventies. Abdullah al-Araby (1967), Nejatullah Siddiqi (1961, 1969), al-Najjar (1971) and Baqir al-Sadr (1961, 1974) were the main contributors.(3)

Early seventies saw the institutional involvement. Conference of the Finance Ministers of the Islamic Countries held in Karachi in 1970, the Egyptian study in 1972, First International Conference on Islamic Economics in Mecca in 1976, International Economic Conference in London in 1977 were the result of such involvement. The involvement of institutions and governments led to the application of theory to practice and resulted in the establishment of the first interest-free banks. The Islamic Development Bank, an inter-governmental bank established in 1975, was born of this process.

4.1.2 The coming into being of interest-free banks

The first private interest-free bank, the Dubai Islamic Bank, was also set up in 1975 by a group of Muslim businessmen from several countries. Two more private banks were founded in 1977 under the name of Faisal Islamic Bank in Egypt and the Sudan. In the same year the Kuwaiti government set up the Kuwait Finance House.

However, small-scale limited scope interest-free banks have been tried before. One in Malaysia in the mid-forties(4) and another in Pakistan in the late-fifties.(5) Neither survived. In 1962 the Malaysian government set up the Pilgrim’s Management Fund to help prospective pilgrims to save and profit.(6) The savings bank established in 1963 at Mit-Ghamr in Egypt was very popular and prospered initially and then closed down for various reasons.(7) However this experiment led to the creation of the Nasser Social Bank in 1972. Though the bank is still active, its objectives are more social than commercial.(8, 9 )

In the ten years since the establishment of the first private commercial bank in Dubai, more than 50 interest-free banks have come into being. Though nearly all of them are in Muslim countries, there are some in Western Europe as well: in Denmark, Luxembourg , Switzerland and the UK. Many banks were established in 1983 (11) and 1984 (13). The numbers have declined considerably in the following years.(10)

In most countries the establishment of interest-free banking had been by private initiative and were confined to that bank. In Iran and Pakistan, however, it was by government initiative and covered all banks in the country. The governments in both these countries took steps in 1981 to introduce interest-free banking. In Pakistan, effective 1 January 1981 all domestic commercial banks were permitted to accept deposits on the basis of profit-and-loss sharing (PLS). New steps were introduced on 1 January 1985 to formally transform the banking system over the next six months to one based on no interest. From 1 July 1985 no banks could accept any interest bearing deposits, and all existing deposits became subject to PLS rules. Yet some operations were still allowed to continue on the old basis. In Iran, certain administrative steps were taken in February 1981 to eliminate interest from banking operations. Interest on all assets was replaced by a 4 percent maximum service charge and by a 4 to 8 percent ‘profit’ rate depending on the type of economic activity. Interest on deposits was also converted into a ‘guaranteed minimum profit.’ In August 1983 the Usury-free Banking Law was introduced and a fourteen-month change over period began in January 1984. The whole system was converted to an interest-free one in March 1985.(11)

4.1.3 The last decade

The subject matter of writings and conferences in the eighties have changed from the concepts and possibilities of interest-free banking to the evaluation of their performance and their impact on the rest of the economy and the world. Their very titles bear testimony to this and the places indicate the world-wide interest in the subject. Conference on Islamic Banking: Its impact on world financial and commercial practices held in London in September 1984, Workshop on Industrial Financing Activities of Islamic Banks held in Vienna in June 1986, International Conference on Islamic Banking held in Tehran in June 1986, International Conference on Islamic Banking and Finance: Current issues and future prospects held in Washington, D.C. in September 1986, Islamic Banking Conference held in Geneva in October 1986, and Conference ‘Into the 1990’s with Islamic Banking‘ held in London in 1988 belong to this category. The most recent one is the Workshop on the Elimination of Riba from the Economy held in Islamabad in April 1992.

Several articles, books and PhD theses have been written on Islamic Banking during this period. Special mention must be made of the work by M. Akram Khan in preparing annotated bibliographies of all published (and some unpublished) works on Islamic Economics (including Islamic Banking) from 1940 and before. It is very useful to students of Islamic Economics and Banking, especially since both English and Urdu works are included (1983, 1991, 1992). M.N. Siddiqi’s bibliographies include early works in Arabic, English and Urdu (1980, 1988). Turkish literature is found in Sabahuddin Zaim (1980).

4.2 Current practices

Generally speaking, all interest-free banks agree on the basic principles. However, individual banks differ in their application. These differences are due to several reasons including the laws of the country, objectives of the different banks, individual bank’s circumstances and experiences, the need to interact with other interest-based banks, etc. In the following paragraphs, we will describe the salient features common to all banks.

4.2.1 Deposit accounts

All the Islamic banks have three kinds of deposit accounts: current, savings and investment.

4.2.1.1 Current accounts

Current or demand deposit accounts are virtually the same as in all conventional banks. Deposit is guaranteed.

4.2.1.2 Savings accounts

Savings deposit accounts operate in different ways. In some banks, the depositors allow the banks to use their money but they obtain a guarantee of getting the full amount back from the bank. Banks adopt several methods of inducing their clients to deposit with them, but no profit is promised. In others, savings accounts are treated as investment accounts but with less stringent conditions as to withdrawals and minimum balance. Capital is not guaranteed but the banks take care to invest money from such accounts in relatively risk-free short-term projects. As such lower profit rates are expected and that too only on a portion of the average minimum balance on the ground that a high level of reserves needs to be kept at all times to meet withdrawal demands.

4.2.1.3 Investment account

Investment deposits are accepted for a fixed or unlimited period of time and the investors agree in advance to share the profit (or loss) in a given proportion with the bank. Capital is not guaranteed.

4.2.2 Modes of financing

Banks adopt several modes of acquiring assets or financing projects. But they can be broadly categorised into three areas: investment, trade and lending.

4.2.2.1 Investment financing

This is done in three main ways: a) Musharaka where a bank may join another entity to set up a joint venture, both parties participating in the various aspects of the project in varying degrees. Profit and loss are shared in a pre-arranged fashion. This is not very different from the joint venture concept. The venture is an independent legal entity and the bank may withdraw gradually after an initial period. b) Mudarabha where the bank contributes the finance and the client provides the expertise, management and labour. Profits are shared by both the partners in a pre-arranged proportion, but when a loss occurs the total loss is borne by the bank. c) Financing on the basis of an estimated rate of return. Under this scheme, the bank estimates the expected rate of return on the specific project it is asked to finance and provides financing on the understanding that at least that rate is payable to the bank. (Perhaps this rate is negotiable.) If the project ends up in a profit more than the estimated rate the excess goes to the client. If the profit is less than the estimate the bank will accept the lower rate. In case a loss is suffered the bank will take a share in it.

4.2.2.2 Trade financing

This is also done in several ways. The main ones are: a) Mark-up where the bank buys an item for a client and the client agrees to repay the bank the price and an agreed profit later on. b) Leasing where the bank buys an item for a client and leases it to him for an agreed period and at the end of that period the lessee pays the balance on the price agreed at the beginning and becomes the owner of the item. c) Hire-purchase where the bank buys an item for the client and hires it to him for an agreed rent and period, and at the end of that period the client automatically becomes the owner of the item. d) Sell-and-buy-back where a client sells one of his properties to the bank for an agreed price payable now on condition that he will buy the property back after certain time for an agreed price. e) Letters of credit where the bank guarantees the import of an item using its own funds for a client, on the basis of sharing the profit from the sale of this item or on a mark-up basis.

4.2.2.3 Lending

Main forms of Lending are: a) Loans with a service charge where the bank lends money without interest but they cover their expenses by levying a service charge. This charge may be subject to a maximum set by the authorities. b) No-cost loans where each bank is expected to set aside a part of their funds to grant no-cost loans to needy persons such as small farmers, entrepreneurs, producers, etc. and to needy consumers. c) Overdrafts also are to be provided, subject to a certain maximum, free of charge.

4.2.3 Services

Other banking services such as money transfers, bill collections, trade in foreign currencies at spot rate etc. where the banks own money is not involved are provided on a commission or charges basis.

4.2.4 Shortcomings in current practices

In the previous section we listed the current practices under three categories: deposits, modes of financing (or acquiring assets) and services. There seems to be no problems as far as banking services are concerned. Islamic banks are able to provide nearly all the services that are available in the conventional banks. The only exception seems to be in the case of letters of credit where there is a possibility for interest involvement. However some solutions have been found for this problem — mainly by having excess liquidity with the foreign bank. On the deposit side, judging by the volume of deposits both in the countries where both systems are available and in countries where law prohibits any dealing in interest, the non-payment of interest on deposit accounts seems to be no serious problem. Customers still seem to deposit their money with interest-free banks.

The main problem, both for the banks and for the customers, seem to be in the area of financing. Bank lending is still practised but that is limited to either no-cost loans (mainly consumer loans) including overdrafts, or loans with service charges only. Both these types of loans bring no income to the banks and therefore naturally they are not that keen to engage in this activity much. That leaves us with investment financing and trade financing. Islamic banks are expected to engage in these activities only on a profit and loss sharing (PLS) basis. This is where the banks’ main income is to come from and this is also from where the investment account holders are expected to derive their profits from. And the latter is supposed to be the incentive for people to deposit their money with the Islamic banks. And it is precisely in this PLS scheme that the main problems of the Islamic banks lie. Therefore we will look at this system more carefully in the following section.

4.3 Problems in implementing the PLS scheme

Several writers have attempted to show, with varying degrees of success, that Islamic Banking based on the concept of profit and loss sharing (PLS) is theoretically superior to conventional banking from different angles. See, for example, Khan and Mirakhor (1987). However from the practical point of view things do not seem that rosy. Our concern here is this latter aspect. In the over half-a-decade of full-scale experience in implementing the PLS scheme the problems have begun to show up. If one goes by the experience of Pakistan as portrayed in the papers presented at the conference held in Islamabad in 1992,(12) the situation is very serious and no satisfactory remedy seems to emerge.(13) In the following paragraphs we will try to set down some of the major difficulties.

4.3.1 Financing

There are four main areas where the Islamic banks find it difficult to finance under the PLS scheme: a) participating in long-term low-yield projects, b) financing the small businessman, c) granting non-participating loans to running businesses, and d) financing government borrowing. Let us examine them in turn.

4.3.1.1 Long-term projects

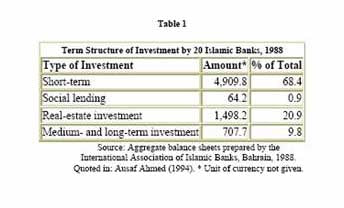

Table 1 (see image below) shows the term structure of investment by 20 Islamic Banks in 1988. It is clear that less than 10 percent of the total assets goes into medium and long-term investment. Admittedly, the banks are unable or unwilling to participate in long-term projects. This is a very unsatisfactory situation.

The main reason of course is the need to participate in the enterprise on a PLS basis which involves time-consuming complicated assessment procedures and negotiations, requiring expertise and experience. The banks do not seem to have developed the latter and they seem to be averse to the former. There are no commonly accepted criteria for project evaluation based on PLS partnerships. Each single case has to be treated separately with utmost care and each has to be assessed and negotiated on its own merits. Other obvious reasons are: a) such investments tie up capital for very long periods, unlike in conventional banking where the capital is recovered in regular instalments almost right from the beginning, and the uncertainty and risk are that much higher, b) the longer the maturity of the project the longer it takes to realise the returns and the banks therefore cannot pay a return to their depositors as quick as the conventional banks can. Thus it is no wonder that the banks are averse to such investments.

4.3.1.2 Small businesses

Small scale businesses form a major part of a country’s productive sector. Besides, they form a greater number of the bank’s clientele. Yet it seems difficult to provide them with the necessary financing under the PLS scheme, even though there is excess liquidity in the banks. The observations of Iqbal and Mirakhor(14) is revealing:

Given the comprehensive criteria to be followed in granting loans and monitoring their use by banks, small-scale enterprises have, in general encountered greater difficulties in obtaining financing than their large-scale counterparts in the Islamic Republic of Iran. This has been particularly relevant for the construction and service sectors, which have large share in the gross domestic product (GDP). The service sector is made up of many small producers for whom the banking sector has not been able to provide sufficient financing. Many of these small producers, who traditionally were able to obtain interest-based credit facilities on the basis of collateral, are now finding it difficult to raise funds for their operations.

4.3.1.3 Running businesses

Running businesses frequently need short-term capital as well l as working capital and ready cash for miscellaneous on-the-spot purchases and sundry expenses. This is the daily reality in the business world. Very little thought seems to have been given to this important aspect of the business world’s requirement. The PLS scheme is not geared to cater to this need. Even if there is complete trust and exchange of information between the bank and the business it is nearly impossible or prohibitively costly to estimate the contribution of such short-term financing on the return of a given business. Neither is the much used mark-up system suitable in this case. It looks unlikely to be able to arrive at general rules to cover all the different situations.

Added to this is the delays involved in authorising emergency loans. One staff member of the Bank of Industry and Mines of Iran has commented:(15)

Often the clients need to have quick access to fresh funds for the immediate needs to prevent possible delays in the project’s implementation schedule. According to the set regulations, it is not possible to bridge-finance such requirements and any grant of financial assistance must be made on the basis of the project’s appraisal to determine type and terms and conditions of the scheme of financing.

The enormity of the damage or hindrance caused by the inability to provide financing to this sector will become clear if we realise that running businesses and enterprises are the mainstay of the country’s very economic survival.

4.3.1.4 Government borrowing

In all countries the Government accounts for a major component of the demand for credit — both short-term and long-term. Unlike business loans these borrowings are not always for investment purposes, nor for investment in productive enterprises. Even when invested in productive enterprises they are generally of a longer-term type and of low yield. This latter only multiplies the difficulties in estimating a rate of return on these loans if they are granted under the PLS scheme. In Iran,(16)

…… it has been decreed that financial transactions between and among the elements of the public sector, including Bank Markazi [the central bank] and commercial banks that are wholly nationalised, can take place on the basis of a fixed rate of return; such a fixed rate is not viewed as interest. Therefore the Government can borrow from the nationalised banking system without violating the Law.

While the last claim may be subject to question, there is another serious consequence:(17)

Continued borrowing on a fixed rate basis by the Government would inevitably index bank charges to this rate than to the actual profits of borrowing entities.

4.3.2 Legislation

Existing banking laws do not permit banks to engage directly in business enterprises using depositors’ funds. But this is the basic asset acquiring method of Islamic banks. Therefore new legislation and/or government authorisation are necessary to establish such banks. In Iran a comprehensive legislation was passed to establish Islamic banks. In Pakistan the Central Bank was authorised to take the necessary steps. In other countries either the banks found ways of using existing regulations or were given special accommodation. In all cases government intervention or active support was necessary to establish Islamic banks working under the PLS scheme.

In spite of this, there is still need for further auxiliary legislation in order to fully realise the goals of Islamic banking. For example, in Pakistan,(18)

… the new law has been introduced without fundamental changes in the existing laws governing contracts, mortgages, and pledges. Similarly no law has been introduced to define modes of participatory financing, that is Musharakah (19) and PTCs. It is presumed that whenever there is a conflict between the Islamic banking framework and the existing law, the latter will prevail. In essence, therefore, the relationship between the bank and the client, that of creditor and debtor is left unchanged as specified by the existing law. …. The existing banking law was developed to protect mainly the credit transactions; its application to other modes of financing results in the treatment of those modes as credit transactions also. Banks doubt whether some contracts, though consistent with the Islamic banking framework, would be acceptable in the courts. Hence, incentives exist for default and abuse.

In Iran, although the law establishing interest-free banking (20)

… is comprehensive, the lack of proper definitions of property rights may have constrained bank lending. Thus far there has been no precise legislative and legal expression of what is viewed as lawful and conditional private property rights. This may also have militated against investment lending in agricultural and industrial sectors and thus encouraged increased concentration of assets in short-term trade financing instruments.

Iran and Pakistan are countries committed to ridding their economies of Riba and have made immense strides in towards achieving it. Yet there are many legal difficulties still to be solved as we have seen above. In other Muslim countries the authorities actively or passively participate in the establishment of Islamic banks on account of their religious persuasion. Such is not the case in non-Muslim countries. Here establishing Islamic banks involves conformation to the existing laws of the concerned country which generally are not conducive to PLS type of financing in the banking sector. We will see some of these problems below.

4.3.3 Involvement in specialised non-bank activities

Dr Hasanuz-Zaman, lists the traditional tasks of the bank and then questions its ability to take on the additional functions it is called upon to perform under the PLS scheme:(21)

It is due to historical reasons that banks have evolved purely as a financial institution. They are suited to attract money, keep it in safe custody, lend it under safety, invest it profitably and enjoy the capacity to create the means of payment. A bank has to maintain a balance between income, liquidity and flexibility. While allocating its funds it has to be meticulously sensitive about the factors like capital position and rate of profitability of various types of loans, stability of deposit, economic conditions, influence of monetary and fiscal policy, ability and experience of banks personnel and credit needs of the area. So far these banks thrive on a fixed rate of return a portion of which is passed on by them to the depositor. Thus the entire effort of a bank is directed towards money management and it is not geared to act as an entrepreneur, trader, industrialist, contractor or caterer.

The question arises: with all these limitations can a bank claim any competence in trading or entrepreneurship which is necessary for musharakah or mudarba (22) contract, or can it act as an owner of a large variety of heavy machinery, transport vehicles or real estate to take the position of a lessor or, can it act as a stockist to buy and resell the entire stock of imports and exports that are needed by genuine traders?

Then he raises the even more serious question:

In case the bank is historically and practically not competent to do all these jobs its claim to share a portion of profits as a working partner, trader or lessor becomes questionable.

Traditional banks do perform a certain amount of project evaluation when granting large medium and long-term loans. But doing such detailed evaluation as would be required to embark on a PLS scheme, such as determining the rates of return and their time schedule, is beyond the scope of conventional banks. So is the detailed accounting and monitoring necessary to determine the actual performance.

Under Islamic banking these exercises are not limited to relatively few large loans but need to be carried out on nearly all the advances made by the bank. Yet, widely acceptable and reliable techniques are yet to be devised. This is confounded by the fact that no consensus has yet been reached on the principles. Both the unprecedented nature of the task as well as the huge amount of work that need be done and the trained and experienced personnel needed to carry them out seems a daunting prospect.

4.3.4 Re-training of staff

As was seen in the previous section, the bank staff will have to acquire many new skills and learn new procedures to operate the Islamic banking system. This is a time-consuming process which is aggravated by two other factors. One, the sheer number of persons that need to be re-trained and, two, the additional staff that need to be recruited and trained to carry out the increased work.

Principles are still to be laid down and techniques and procedures evolved to carry them out. It is only after the satisfactory achievement of these that proper training can begin. This delay and the resulting confusion appears to be among the main reasons for the banks to stick to modes of financing that are close to the familiar interest-based modes.

4.3.5 Other disincentives

Among the other disincentives from the borrower’s point of view are the need to disclose his accounts to the bank if he were to borrow on the PLS basis, and the fear that eventually the tax authorities will become wise to the extent of his business and the profits. Several writers have lashed out at the lack of business ethics among the business community, but that is a fact of life at least for the foreseeable future. There is a paucity of survey or case studies of clients to see their reaction to current modes of financing. As such we are not aware of further disincentives that might be there.

4.3.5.1 Accounts

When a business is financed under the PLS scheme it is necessary that the actual profit/loss made using that money be calculated. Though no satisfactory methods have yet been devised, the first requirement for any such activity is to have the necessary accounts. On the borrowers side there are two difficulties: one, many small-time businessmen do not keep any accounts, leave alone proper accounts. The time and money costs will cut into his profits. Larger businesses do not like to disclose their real accounts to anybody. On the banks’ side the effort and expense involved in checking the accounts of many small accounts is prohibitive and will again cut into their own share of the profits. Thus both sides would prefer to avoid having to calculate the actually realised profit/loss. To quote Iqbal and Mirakhor:(23)

…. the commercial banks do face an element of moral hazard owing to the non-existence of systematic book-keeping in this sector. Additionally the reluctance of small producers to submit their operations to bank audits and the perceived enormous cost of auditing and monitoring relative to the small size of the potential credits makes banks unwilling to extend credit on the basis of new modes of financing to these small producers. These reduced lending to small producers may also explain the existence of excess liquidity in the banking system.

4.3.5.2 Tax

The bank is a big business and it has to declare its profit and loss and is legally required to present an audited account of its operations. Once the bank’s accounts are known it doesn’t take much for the tax collectors to figure out the share of the businesses financed by the bank under the PLS scheme. Thus it’s no surprise that businesses are not too very happy about the situation. The fact that suggestions have been made to use the banks to collect taxes due has not helped the matter either.

4.3.6 Excess liquidity

Presence of excess liquidity is reported in nearly all Islamic banks. This is not due to reduced demand for credit but the due to the inability of the banks to find clients willing to be funded under the new modes of financing. Some of these difficulties are mentioned under section 4.3.1 Financing. Here we have a situation where there is money available on the one hand and there is need for it on the other but the new rules stand in the way of bringing them together! This is a very strange situation — specially in the developing Muslim countries where money is at a premium even for ordinary economic activities, leave alone development efforts. Removal of riba was expected to ease such difficulties, not to aggravate the already existing ones!

4.3.7 Uneasy questions of morality

The practices in use by the Islamic banks have evoked questions of morality. Do the practices adopted to avoid interest really do their job or is it simply a change of name? It suffices to quote a few authors. (24)

The Economist writes: (25)

….. Muslim theoreticians and bankers have between them devised ingenious ways of coping with the interest problem. One is murabaha. The Koran says you cannot borrow $100m from the bank for a year, at 5% interest, to buy the new machinery your factory needs? Fine. You get the bank to buy the machinery for you — cost, $100m — and then you buy the stuff from the bank, paying it $105m a year from now. The difference is that the extra $5m is not interest on loan, which the Koran (perhaps) forbids, but your thanks to the bank for the risk it takes of losing money while it is the owner of the machinery: this is honest trading, okay with the Koran. Since with modern communications the bank’s ownership may last about half a second, its risk is not great, but the transaction is pure. It is not surprising that some Muslims uneasily sniff logic-chopping here.

Dr Ghulam Qadir says of practices in Pakistan: (26)

Two of the modes of financing prescribed by the State Bank, namely financing through the purchase of client’s property with a buy-back agreement and sale of goods to clients on a mark-up, involved the least risk and were closest to the old interest-based operations. Hence the banks confined their operations mostly to these modes, particularly the former, after changing the simple buy-back agreement (prescribed by the State Bank) to buy-back agreement with a mark-up, as otherwise there was no incentive for them to extend any finances. The banks also reduced their mark-up-based financing, whether through the purchase of client’s property or through the sale of goods to clients, to mere paper work, instead of actual buying of goods (property), taking their possession and then selling (back) to the client. As a result, there was no difference between the mark-up as practised by the banks and the conventional interest rate, and hence it was judged repugnant to Islam in the recent decision of the Federal Shari’ah court.

As banks are essentially financial institutions and not trading houses, requiring them to undertake trading in the form of buy-back arrangements and sale on mark-up amounts to imposing on them a function for which they are not well equipped. Therefore, banks in Pakistan made such modifications in the prescribed modes which defeated the very purpose of interest-free financing. Furthermore, as these two minimum-risk modes of financing were kept open to banks, they never tried to devise innovative and imaginative modes of financing within the framework of musharakah and mudarba.

Prof. Khurshid Ahmad says: (27)

Murabaha (cost-plus financing) and bai- mu’ajjal (sale with deferred payment) are permitted in the Shari’ah under certain conditions. Technically, it is not a form of financial mediation but a kind of business participation. The Shari’ah assumes that the financier actually buys the goods and then sells them to the client. Unfortunately, the current practice of “buy-back on mark-up” is not in keeping with the conditions on which murabaha or bai- mu’ajjal are permitted. What is being done is a fictitious deal which ensures a predetermined profit to the bank without actually dealing in goods or sharing any real risk. This is against the letter and spirit of Shari’ah injunctions.

While I would not venture a fatwa, as I do not qualify for that function, yet as a student of economics and Shari’ah I regard this practice of “buy-back on mark-up” very similar to riba and would suggest its discontinuation. I understand that the Council of Islamic Ideology has also expressed a similar opinion.

Dr Hasanuz Zaman is more scathing in his condemnation: (28)

It emerges that practically it is impossible for large banks or the banking system to practise the modes like mark-up, bai- salam, buy-back, murabaha, etc. in a way that fulfils the Shari’ah conditions. But in order to make themselves eligible to a return on their operations, the banks are compelled to play tricks with the letters of the law. They actually do not buy, do not posses, do not actually sell and deliver the goods; but the transition is assumed to have taken place. By signing a number of documents of purchase, sale and transfer they might fulfil a legal requirement but it is by violating the spirit of prohibition.

Again, (29)

It seems that in large number of cases the ghost of interest is haunting them to calculate a fixed rate percent per annum even in musharakah, mudarba, leasing, hire-purchase, rent sharing, murabaha, (bai- mu’ajjal, mark-up), PTC, TFC, (30) etc. The spirit behind all these contracts seems to make a sure earning comparable with the prevalent rate of interest and, as far as possible, avoid losses which otherwise could occur.

To sum up, in Dr Hasanuz Zaman’s words: (31)

… many techniques that the interest-free banks are practising are not either in full conformity with the spirit of Shari’ah or practicable in the case of large banks or the entire banking system. Moreover, they have failed to do away with undesirable aspects of interest. Thus, they have retained what an Islamic bank should eliminate.

4.4 Islamic banking in non-Muslim countries

The modern commercial banking system in nearly all countries of the world is mainly evolved from and modelled on the practices in Europe, especially that in the United Kingdom. The philosophical roots of this system revolves around the basic principles of capital certainty for depositors and certainty as to the rate of return on deposits. In order to enforce these principles for the sake of the depositors and to ensure the smooth functioning of the banking system Central Banks have been vested with powers of supervision and control. All banks have to submit to the Central Bank rules. Islamic banks which wish to operate in non-Muslim countries have some difficulties in complying with these rules. We will examine below the salient features.(32)

4.4.1 Certainty of capital and return

While the conventional banks guarantee the capital and rate of return, the Islamic banking system, working on the principle of profit and loss sharing, cannot, by definition, guarantee any fixed rate of return on deposits. Many Islamic banks do not guarantee the capital either, because if there is a loss it has to be deducted from the capital. Thus the basic difference lies in the very roots of the two systems. Consequently countries working under conventional laws are unable to grant permission to institutions which wish to operate under the PLS scheme to functions as commercial banks. Two official comments, one from the UK and the other from the USA suffice to illustrate this.

Sir Leigh Pemberton, the Governor of the Bank of England, told the Arab Bankers’ Association in London that: (33)

It is important not to risk misleading and confusing the general public by allowing two essentially different ban king systems to operate in parallel;

A central feature of the banking system of the United Kingdom as enshrined in the legal framework is capital certainty for depositors. It is the most important feature which distinguished the banking sector from the other segments of the financial system;

Islamic banking is a perfectly acceptable mode of financing but it does not fall within the definition of what constitutes banking in the UK;

The Bank of England is not legally able to authorise under the Banking Act, an institution which does not take deposits as defined under that Act;

The Islamic facilities might be provided within other areas of the financial system without using a banking name.

In the United States, Mr Charles Schotte, the US Treasury Department specialist in regulatory issues has remarked: (34)

There has never been an application for an Islamic establishment to set up either as a bank or as anything else. So there is no precedent to guide us. Any institution that wishes to use the word ‘bank’ in its title has to guarantee at least a zero rate of interest — and even that might contravene Islamic laws.

4.4.2 Supervision and control

Besides these, there are other concerns as well. One is the Central Bank supervision and control. This mainly relates to liquidity requirements and adequacy of capital. These in turn depend on an assessment of the value of assets of the Islamic banks. A financial advisor has this to say: (35)

The bank of England, under the 1979 Act, would have great difficulty in putting a value on the assets of an Islamic institution which wanted to operate as a bank in the UK. The traditional banking system has much of its assets in fixed interest instruments and it is comparatively easy to value that. For example, if they are British Government instruments they will have a quoted market value; and there are recognised methods for valuing traditional banking assets when they become non-productive. But it is very difficult indeed to value an Islamic asset such as a share in a joint venture; and the Bank of England would have to send a team of experienced accountants into every Islamic bank operating in the UK as a bank under the 1979 Act, to try to put a proper and cautious value on its assets.

Another financial analyst states: (36)

Even if a method could be found for assessing the risks to calculate the capital necessary, little comfort could be taken from the profitability which is usually relied upon to cover day-to-day losses arising from the bank’s business, because a substantial part of an Islamic bank’s portfolio is venture capital without any guaranteed return.

It is evident then that even if there is a desire to accommodate the Islamic system, the new procedures that need be developed and the modifications that need be made to existing procedures are so large that the chances of such accommodation in a cautious sector such as banking is very remote indeed. Any relaxation of strict supervision is precluded because should an Islamic bank fail it would undermine the confidence in the whole financial system, with which it is inevitably identified. As Suratgar puts it: (37)

There could be potential dangers for the international system, where the failure of such an institution could bring with it the failure of other associated institutions, or of all the Western banking institutions which come closely tied to with such an operation.

The question has engaged the attention of Central Banks in Muslim countries as well. But reliable satisfactory methods are still to developed.

4.4.3 Tax regulations

Another important consideration is the tax procedures in non-Muslim countries. While interest is a ‘passive’ income, profit is an earned income which is treated differently. In addition, in trade financing there are title transfers twice — once from seller to bank and then from bank to buyer — and therefore twice taxed on this account decreasing the profitability of the venture. The Director of the International Islamic Bank of Denmark says: (38)

Tax laws are against the Islamic philosophy and pose the greatest difficulty. In most OECD countries Mudarabha is constrained by fiscal acts which define profits as an after tax item for the profit creator and a fully taxable item for the profit receiver.

4.5 Discussion and suggestions

People have needs — food, clothes, houses, machinery, services; the list is endless. Entrepreneurs perceive these needs and develop ways and means of catering to them. They advertise their products and services, peoples expectations are raised and people become customers of the entrepreneur. If the customers needs are fulfilled according to their expectations they continue to patronise the entrepreneur and his enterprise flourishes. Otherwise his enterprise fails and people take to other entrepreneurs.

Banks too are enterprises; they cater to peoples’ needs connected with money — safe-keeping, acquiring capital, transferring funds etc. The fact that they existed for centuries and continue to exist and prosper is proof that their methods are good and they fulfil the customers needs and expectations. Conventional commercial banking system as it operates today is accepted in all countries except the Islamic world where it is received with some reservation. The reservation is on account of the fact that the banking operations involve dealing in interest which is prohibited in Islam. Conventional banks have ignored this concern on the part of their Muslim clientele. Muslims patronised the conventional banks out of necessity and, when another entrepreneur — the Islamic banker — offered to address their concern many Muslims turned to him. The question is: has the new entrepreneur successfully met their concerns, needs and expectations? If not he may have to put up his shutters!

Broadly speaking, banks have three types of different customers: depositors, borrowers and seekers of bank’s other services such as money transfer. Since services do not generally involve dealing in interest Muslims have no problem transacting such businesses with conventional banks; neither do Islamic banks experience any problems in providing these services. Among the depositors there are current account holders who too, similarly, have no problems. It is the savings account holders and the borrowers who have reservations in dealing with the conventional banks. In the following paragraphs we will see how well the Islamic banks have succeeded in addressing their customers’ special concern.

4.5.1 Savings accounts and capital guarantee

As pointed out earlier, our concern here is the savings account holders. As the name itself indicates the primary aim of the saving account depositor is the safe-keeping of his savings. It is correctly perceived by the conventional banker and he guarantees the return of the deposit in total. The banker also assumes that the depositor will prefer to keep his money with him in preference to another who might also provide the same guarantee if the depositor is provided an incentive. This incentive is called interest, and this interest is made proportional to the amount and length of time it is left with the bank in order to encourage more money brought into the bank and left there for longer periods of time. In addition, the interest rate is fixed in advance so that the depositor and the banker are fully aware of their respective rights and obligations from the beginning. And laws have been enacted to guarantee their enforcement. In Economic theory the interest is often taken to be the compensation the depositors demand and receive for parting with their savings. The fact that the depositors accept the paid interest and that, given other things being equal, they prefer the bank or the scheme which offers the highest interest proves the banker’s assumption correct.

The scheme is simple, transparent and seems to have satisfied the requirements of all types of savers — from teenagers to old-age pensioners, from individuals to large institutions, pension funds and endowments, from small amounts to millions, and from a few weeks or months to years — that it has survived over centuries and operates across national, cultural and religious borders.

The situation is very different in the Islamic banks. Here to the depositor’s first aim is to keep his savings in safe custody. Islamic bankers divide the conventional savings account into two categories (alternatively, create a new kind of account): savings account and investment account. The investment accounts operate fully under the PLS scheme — capital is not guaranteed, neither is there any pre-fixed return. Under the savings account the nominal value of the deposit is guaranteed, but they receive no further guaranteed returns. (39) Banks may consider funds under the savings accounts too as part of their resources and use it to create assets. This is theory. In practice, however, the banks prefer, encourage and emphasise the investment accounts. This is because since their assets operate under the PLS scheme they might incur losses on these assets which losses they cannot pass onto the savings accounts depositors on account of the capital guarantee on these accounts. In the process the first aim of the depositor is pushed aside and the basic rule of commercial banking –capital guarantee– is broken.(40)

It is suggested that all Islamic banks guarantee the capital under their savings accounts. This will satisfy the primary need and expectation of an important section of the depositors and, in Muslim countries where both Islamic and conventional banks co-exist, will induce more depositors to bank with the Islamic banks. At the same time, it will remove the major objection to establishing Islamic banks in non-Muslim countries.

But the question is how does the bank make an income from these deposits? We will examine this in the next section.

4.5.2 Loans with a service charge

We have already seen that all the problems of the Islamic banks arise from their need to acquire their assets under the PLS scheme. A simple solution does, in fact, already exist in the current theories of Islamic banking. It need only be pointed out and acted upon. We will examine the provisions in the Iranian, Pakistani and the Siddiqi models. (41)

All three models provide for loans with a service charge. Though the specific rules are not identical, the principle is the same. We suggest that the funds in the deposit accounts (current and savings) be used to grant loans (short and long-term) with a service charge. By doing this the Islamic banks will be able to provide all the loan facilities that conventional banks provide while giving capital guarantee for depositors and earning an income for themselves. Furthermore, and it is important, they can avoid all the problems discussed in section 4.3. This would also remove the rest of the obstacles in opening and operating Islamic banks in non-Muslim countries.

The bonus for the borrowers is that the service charge levied by the Islamic banks will necessarily be less than the interest charged by conventional banks.

Let us now look at the existing relevant rules in the three models. The Iranian model provides for Gharz-al hasaneh whose definition, purpose and operation are given in Articles 15, 16 and 17 of Regulations relating to the granting of banking facilities:(42)

Article 15

Gharz-al-hasaneh is a contract in which one (the lender) of the two parties relinquishes a specific portion of his possessions to the other party (the borrower) which the borrower is obliged to return to the lender in kind or, where not possible, its cash value.

Article 16

… the banks … shall set aside a part of their resources and provide Gharz-al-hasaneh for the following purposes:

(a) to provide equipment, tools and other necessary resources so as to enable the creation of employment, in the form of co-operative bodies, for those who lack the necessary means;

(b) to enable expansion in production, with particular emphasis on agricultural, livestock and industrial products;

(c) to meet essential needs.

Article 17

The expenses incurred in the provision of Gharz-al-hasaneh shall be, in each case, calculated on the basis of the directives issued by Bank Markazi Jomhouri Islami Iran (43) and collected from the borrower.

In Pakistan, permissible modes of financing include: (44)

Financing by lending:

(i) Loans not carrying any interest on which the banks may recover a service charge not exceeding the proportionate cost of the operation, excluding the cost of funds and provisions for bad and doubtful debts. The maximum service charge permissible to each bank will be determined by the State Bank from time to time.

(ii) Qard-e-hasana loans given on compassionate grounds free of any interest or service charge and repayable if and when the borrower is able to pay.

Siddiqi has suggested that 50 percent of the funds in the ‘loan’ (i.e. current and savings) accounts be used to grant short-term loans.(45) A fee is to be charged for providing these loans: (46)

An appropriate way of levying such a fee would be to require prospective borrowers to pay a fixed amount on each application, regardless of the amount required, the term of the loan or whether the application is granted or rejected. Then the applicants to whom a loan is granted may be required to pay an additional prescribed fee for all the entries made in the banks registers. The criterion for fixing the fees must be the actual expenditure which the banks have incurred in scrutinising the applications and making decisions, and in maintaining accounts until loans are repaid. These fees should not be made a source of income for the banks, but regarded solely as a means of maintaining and managing the interest-free loans.

It is clear from the above that all three models agree on the need for having cash loans as one mode of financing, and that this service should be paid for by the borrower. Though the details may vary, all seem to suggest that the charge should be the absolute cost only. We suggest that a percentage of this absolute cost be added to the charge as a payment to the bank for providing this service. This should enable an Islamic bank to exist and function independently of its performance in its PLS operations.

4.5.3 Investment under PLS scheme

The idea of participatory financing introduced by the Islamic banking movement is a unique and positive contribution to modern banking. However, as we saw earlier, by making the PLS mode of financing the main (often almost the only) mode of financing the Islamic banks have run into several difficulties. If, as suggested in the previous section, the Islamic banks would provide all the conventional financing through lending from their deposit accounts (current and savings), it will leave their hands free to engage in this responsible form of financing innovatively, using the funds in their investment accounts. They could then engage in genuine Mudaraba financing. Being partners in an enterprise they will have access to its accounts, and the problems associated with the non-availability of accounts will not arise.

Commenting on Mudaraba financing, The Economist says:(47)

…. some people in the West have begun to find the idea attractive. It gives the provider of money a strong incentive to be sure he is doing something sensible with it. What a pity the West’s banks did not have that incentive in so many of their lending decisions in the 1970s and 1980s. It also emphasises the sharing of responsibility, by all the users of money. That helps to make the free-market system more open; you might say more democratic.

4.6 Conclusions

Islamic banking is a very young concept. Yet it has already been implemented as the only system in two Muslim countries; there are Islamic banks in many Muslim countries, and a few in non-Muslim countries as well. Despite the successful acceptance there are problems. These problems are mainly in the area of financing.

With only minor changes in their practices, Islamic banks can get rid of all their cumbersome, burdensome and sometimes doubtful forms of financing and offer a clean and efficient interest-free banking. All the necessary ingredients are already there. The modified system will make use of only two forms of financing — loans with a service charge and Mudaraba participatory financing — both of which are fully accepted by all Muslim writers on the subject.

Such a system will offer an effective banking system where Islamic banking is obligatory and a powerful alternative to conventional banking where both co-exist. Additionally, such a system will have no problem in obtaining authorisation to operate in non-Muslim countries.

Participatory financing is a unique feature of Islamic banking, and can offer responsible financing to socially and economically relevant development projects. This is an additional service Islamic banks offer over and above the traditional services provided by conventional commercial banks.

Notes:

1 Rad (1991), pp.3-4.

2 Siddiqi (1980), pp.219-20.

3 ibid. p.222.

4 Arabia, April 1982, No.8; p.46

5 Wilson (1984)

6 Arabia, April 1982, No.8; p.46

7 Wilson (1984)

8 ibid.

9 All quoted in Rad (1991). p.13-14.

10 Ausaf Ahmed (1994). p.373.

11 Iqbal and Mirakhor (1987).

12 Elimination of Riba from the Economy. Islamabad: IPS, 1994.

13 At present the author has no information as to the recent situation in Iran.

14 ibid. p.24.

15 Quoted in: Rad (1991). p.56.

16 Iqbal and Mirakhor (1987). p.24.

17 ibid. p.24.

18 ibid. p.25.

19 Musharakah and Musharaka are different English spellings of the same Arabic word.

20 ibid. p.25.

21 Zaman (1994). p.204.

22 Mudarba, Mudarabha and Mudaraba are different English spellings of the same Arabic word.

23 ibid. p.25.

24 Italics are mine

25 The Economist (1994). p.9.

26 Qadir (1994). p.105.

27 Ahmad (1994). p.46-47.

28 Zaman (1994). p.208.

29 ibid. p.203.

30 PTC (participation term certificate) and TFC (term finance certificate) are the two Pakistani instruments to provide long-, medium- and short-term finance.

31 ibid. p.212.

32 All quotations in this section appear in Rad (1991).

33 Pemberton (1984)

34 Schotta (1985)

35 Steele (1984)

36 Suratgar (1984)

37 ibid. p.30.

38 Karsten (1982) p.120.

39 It should be noted that early writers such as Mawdudi (1961) and Siddiqi (1968) conceived of savings accounts with capital guarantee. In the Iranian model too capital is guaranteed. The Law for Usury- (Interest) free Banking (August 1983), Chapter II, article 4. In Pakistan, however, … all deposits accepted by a banking company shall be on the basis of participation in profit and loss of the banking company, except deposits received in Current Account … State Bank of Pakistan, BCD Circular No 13, 20 June 1984. See Appendix in Iqbal and Mirakhor (1987), pp.36-37.

40 We are at present not aware of any survey or case studies of depositors which would enable us to assess their reaction to this state of affairs.

41 Laws and regulations relating to interest-free banking in Iran and Pakistan are reproduced in Iqbal and Mirakhor (1987), pp.31-58. Siddiqi (1988).

42 Iqbal and Mirakhor (1987), pp.36-37.

43 Central Bank of the Islamic Republic of Iran.

44 Iqbal and Mirakhor (1987), p.45.

45 the other 10 and 40 percent respectively are to be used for cash reserve and mudaraba investment.

46 Siddiqi (1988), p.69.

47 op cit. p.9-10.

To read more of Professor A.L.M. Abdul Gafoor’s articles, go to: http://users.bart.nl/~abdul/chap4.html

PrintPinterestShare

Leave a comment

Also in FINANCE & ECONOMICS

Recent History of Islamic Banking and Finance

The Foundations of Islamic Finance

During the short span of a quarter century, a new way of financial intermediation and investment management emerged and gained a sizeable part of the market – between a fourth and a third – in its home base, the Persian Gulf countries. During the same period it spread far and wide reaching Malaysia and Indonesia in the east and the Americas in the west, and a number of Muslim countries adopted the new system at the state level.

It is interesting to ask why it emerged, how it works, what sustains it and what are its potentialities for you and me and the humanity at large. The query is timely as all is not well with our conventional system of money, banking and finance. It has become increasingly unstable, facing recurrent crises. It has failed to help in reducing the increasing gap between the rich and the poor, within nations and between nations. Many think it is partly responsible for increasing inequality.

Problems and Prospects of Islamic Banking and Finance

During the last few decades of the twentieth century, the period in which Islamic banking and financial institutions were evolving, great changes were taking place in the financial environment. In this lecture I will examine the problems and prospects of Islamic banking in the perspective of these changes. Two changes are most significant, decline in intermediation and resort to more active, rather aggressive management of investment, and world-wide integration of financial markets in the wake of globalization.

The first trend, symbolized by the repeal of Glass-Steagal in the United States, should be advantageous to Islamic finance insofar as financial intermediation was based on interest. Greater involvement of banks/financial institutions in investment management afforded wider scope for using the Islamic financial techniques of profit-sharing, mark up financing, etc.

Collecting

Learn More

Contact | Ali Omar Ermes

Thank you for visiting.

We welcome your comments and suggestions.

Ali Omar Ermes

News & Updates

Join our Newsletter for exclusive discounts, new releases and more

© 2026 Ali Omar Ermes. All Rights Reserved.